Tax Deduction on Signing Money Payments from Real Estate Developers to Landowners – 2025 Guide

রিয়েল এস্টেট উন্নয়নকারীর (ডেভেলপার) নিকট হতে ভূমির মালিক কর্তৃক প্রাপ্ত আয়ের উপর কর কর্তন – বিস্তারিত ব্যাখ্যা

Legal Context

Under the Income Tax Act of Bangladesh, there are specific provisions regarding Tax Deduction at Source (TDS) when a real estate developer (land developer) makes any payment to a landowner in exchange for land development or under a joint venture/power of attorney arrangement.

This falls under the rule often known as “tax deduction on signing money or consideration for development rights”, typically governed by the Third Schedule or relevant SROs issued by the National Board of Revenue (NBR).

আইনি ভিত্তি

বাংলাদেশের আয়কর আইন, 2023 অনুযায়ী, যখন কোনো রিয়েল এস্টেট ডেভেলপার বা ভূমি উন্নয়নকারী প্রতিষ্ঠান কোনো ভূমির মালিককে উন্নয়নের উদ্দেশ্যে অর্থ প্রদান করে — তখন সেই অর্থের উপর উৎসে কর (Tax Deduction at Source – TDS) কর্তন করতে হয়।

এই বিধানটি মূলত ভূমি উন্নয়ন ও যৌথ উন্নয়ন (Joint Venture) প্রকল্পগুলিতে প্রযোজ্য, যেখানে ডেভেলপার ভূমি মালিকের কাছ থেকে Power of Attorney বা চুক্তিপত্রের মাধ্যমে জমির উন্নয়নের অধিকার পায়।

Who Are the Parties Involved?

Landowner – The person who owns the land.

Developer / Real Estate Company – The person or company engaged in real estate or land development business who enters into a development agreement or receives Power of Attorney from the landowner to construct and sell flats or apartments.

কারা এর অন্তর্ভুক্ত

ভূমির মালিক (Landowner) – যিনি জমির মালিক।

ডেভেলপার বা ভূমি উন্নয়নকারী প্রতিষ্ঠান (Developer) – যে প্রতিষ্ঠান বা ব্যক্তি জমি উন্নয়নের ব্যবসার সাথে যুক্ত এবং উন্নয়নের জন্য মালিকের সঙ্গে চুক্তি করে।

When Does This Provision Apply?

This tax rule applies whenever a developer or land development company makes any payment to a landowner for development purposes — no matter what the payment is called.

The payment may be titled as:

Signing money

Advance money

Subsistence money

Land value or partial land price

House rent

Any other payment in cash, cheque, or transfer under Power of Attorney or development agreement

Even if the agreement has a different name or format, as long as it involves transferring or using land for development, this provision applies.

কখন কর কর্তন করতে হবে

যখনই কোনো ডেভেলপার ভূমির মালিককে উন্নয়ন সংক্রান্ত যে কোনো নামে অর্থ প্রদান করবে, তখনই কর কর্তন করতে হবে।

অর্থ প্রদানের নাম যাই হোক না কেন, যেমন—

সাইনিং মানি (Signing Money)

পণমূল্য / subsistence money

অগ্রিম অর্থ / advance

বাড়ি ভাড়া

বা অন্য কোনো নামে অর্থ প্রদান

যদি অর্থ প্রদানটি ভূমি উন্নয়ন বা রিয়েল এস্টেট প্রকল্পের অংশ হয়, তবে সেই অর্থ প্রদানের সময়েই কর কর্তন প্রযোজ্য।

Key Points to Note

- The developer is legally responsible for deducting and depositing the tax.

- The deducted tax is adjustable against the landowner’s annual income tax liability.

- The TDS certificate must be issued to the landowner as proof of deduction.

কর জমা ও সার্টিফিকেট

- কর্তনকৃত অর্থ জাতীয় রাজস্ব বোর্ড (NBR)-এর নির্ধারিত ট্রেজারি কোড এর মাধ্যমে জমা দিতে হয়।

- কর জমা দেওয়ার পর ডেভেলপারকে TDS সার্টিফিকেট (উৎসে কর কর্তন সনদ) ভূমির মালিককে দিতে হবে।

- এই কর্তনকৃত কর পরবর্তীতে ভূমির মালিকের বাৎসরিক আয়কর রিটার্নে সমন্বয় (adjust) করা যায়।

Purpose of the Provision

This rule exists to:

- Ensure that income derived from real estate development is properly taxed at the source.

- Prevent tax evasion through undeclared payments in land development projects.

- Promote transparency between landowners and developers.

এই বিধানের উদ্দেশ্য

এই নিয়মের মূল উদ্দেশ্য হলো—

- ভূমি উন্নয়ন বা রিয়েল এস্টেট খাতে আয়ের সঠিক কর আদায় নিশ্চিত করা।

- অঘোষিত বা নগদ লেনদেনের মাধ্যমে কর ফাঁকি রোধ করা।

- ভূমির মালিক ও ডেভেলপারের মধ্যে স্বচ্ছতা বজায় রাখা।

In Summary

| Particular | Description |

|---|---|

| Who pays the tax? | Developer (by deducting at source) |

| Who bears the tax? | Landowner (it’s the landowner’s income) |

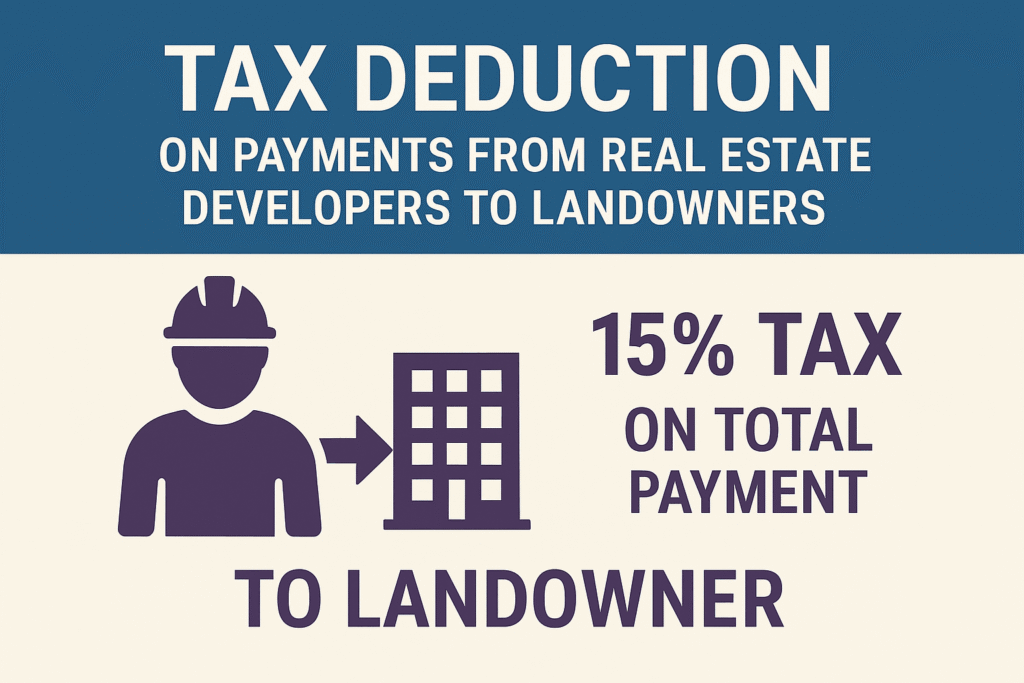

| Rate of tax deduction | 15% on the total payment |

| When deducted? | At the time of making or crediting the payment |

| Legal basis | NBR rules on tax deduction from payments to landowners by developers |

| Purpose | To collect tax in advance on income arising from land development or real estate transactions |

সংক্ষেপে সারাংশ

| বিষয় | বিবরণ |

|---|---|

| কর্তন করবে কে | ডেভেলপার |

| কর বহন করবে কে | ভূমির মালিক |

| হার | ১৫% |

| কর্তনের সময় | অর্থ প্রদান বা ক্রেডিট করার সময় |

| জমা দেওয়ার স্থান | NBR কোষাগার |

| উদ্দেশ্য | ভূমি উন্নয়নজনিত আয়ের উপর উৎসে কর সংগ্র |

115. Tax shall be deducted from the income received by the landowner from the real estate developer, including land.

In any case where any person engaged in the business of real estate or land development, by virtue of a power of attorney, agreement, or any written contract, makes any payment to the landowner—whether such payment is termed as signing money, subsistence money, house rent, or any other name whatsoever—for the purpose of developing land owned by an individual or a business entity, income tax at the rate of 15% (fifteen percent) shall be deducted at the time of making such payment on the total amount so paid.

Conclusion

In Bangladesh, the rule under section 115 ensures that any payment made by a real estate developer to a landowner for land development purposes is subject to a 15% tax deduction at source (TDS).

This provision aims to bring transparency to real estate transactions and ensure proper tax collection from income generated through development agreements or power of attorney arrangements.

For both developers and landowners, compliance with this rule is essential to avoid penalties and disputes with the National Board of Revenue (NBR).

Proper documentation, timely tax deduction, and accurate deposit of the deducted amount are the keys to staying compliant and maintaining smooth business operations in the real estate sector.

উপসংহার

বাংলাদেশে আয়কর আইন অনুযায়ী, রিয়েল এস্টেট ডেভেলপার বা ভূমি উন্নয়নকারী প্রতিষ্ঠান কর্তৃক ভূমির মালিককে প্রদত্ত অর্থের উপর ১৫% হারে উৎসে কর (TDS) কর্তন বাধ্যতামূলক।

এই বিধানটির মূল উদ্দেশ্য হলো রিয়েল এস্টেট খাতে স্বচ্ছতা নিশ্চিত করা এবং উন্নয়ন সংক্রান্ত আয় থেকে যথাযথভাবে কর আদায় করা।

ভূমির মালিক ও ডেভেলপার উভয়েরই উচিত এই নিয়ম মেনে চলা—

যাতে জাতীয় রাজস্ব বোর্ড (NBR)-এর সঙ্গে কোনো জটিলতা, জরিমানা বা বিরোধ সৃষ্টি না হয়।

সময়মতো কর কর্তন, জমা ও প্রমাণপত্র সংরক্ষণ করলে রিয়েল এস্টেট ব্যবসা আরও সুশৃঙ্খল ও আইনসম্মতভাবে পরিচালিত হবে।